Gold prices began 2026 on a firm footing, extending momentum from a historic prior year as renewed demand met a softer U.S. dollar. In early Asian trading, spot gold climbed 1.6% to $4,378.55 per ounce, while U.S. gold futures advanced 1.2% to $4,392.40. The gains followed a brief pullback late in December, when prices eased from record highs amid holiday-thinned volumes.

The rebound reflects a familiar dynamic: a weaker dollar and expectations for easier monetary policy revived appetite for bullion. As the greenback slipped, gold became more attractive for investors using other currencies, restoring near-term support just as global markets reopened after year-end closures.

Despite last week’s consolidation, gold remains firmly anchored by structural drivers that dominated 2025. The metal closed the year with a gain of more than 60%, marking one of its strongest annual performances in decades and cementing its role as a core portfolio hedge.

Rate Cuts and Risk Fuelled 2025 Surge

Gold’s exceptional run in 2025 was powered primarily by U.S. monetary policy. The Federal Reserve delivered multiple interest-rate cuts, reducing the opportunity cost of holding non-yielding assets. Markets now expect further easing in 2026, reinforcing gold’s appeal as yields compress across major economies.

Geopolitical risk added a second tailwind. Prolonged conflicts in Eastern Europe and the Middle East sustained safe-haven flows, while broader concerns over global growth and political fragmentation encouraged defensive positioning. Central banks also played a decisive role, with continued official-sector buying, particularly from emerging markets seeking to diversify reserves and reduce dollar exposure.

Key forces supporting gold include:

- Lower real yields following Fed rate cuts

- Persistent geopolitical uncertainty

- Central bank demand at historically high levels

- A softer U.S. dollar boosting global affordability

Although prices retreated modestly from their peaks late last year, analysts argue the foundations of the rally remain intact as 2026 begins.

Silver and Platinum Extend Strong Momentum

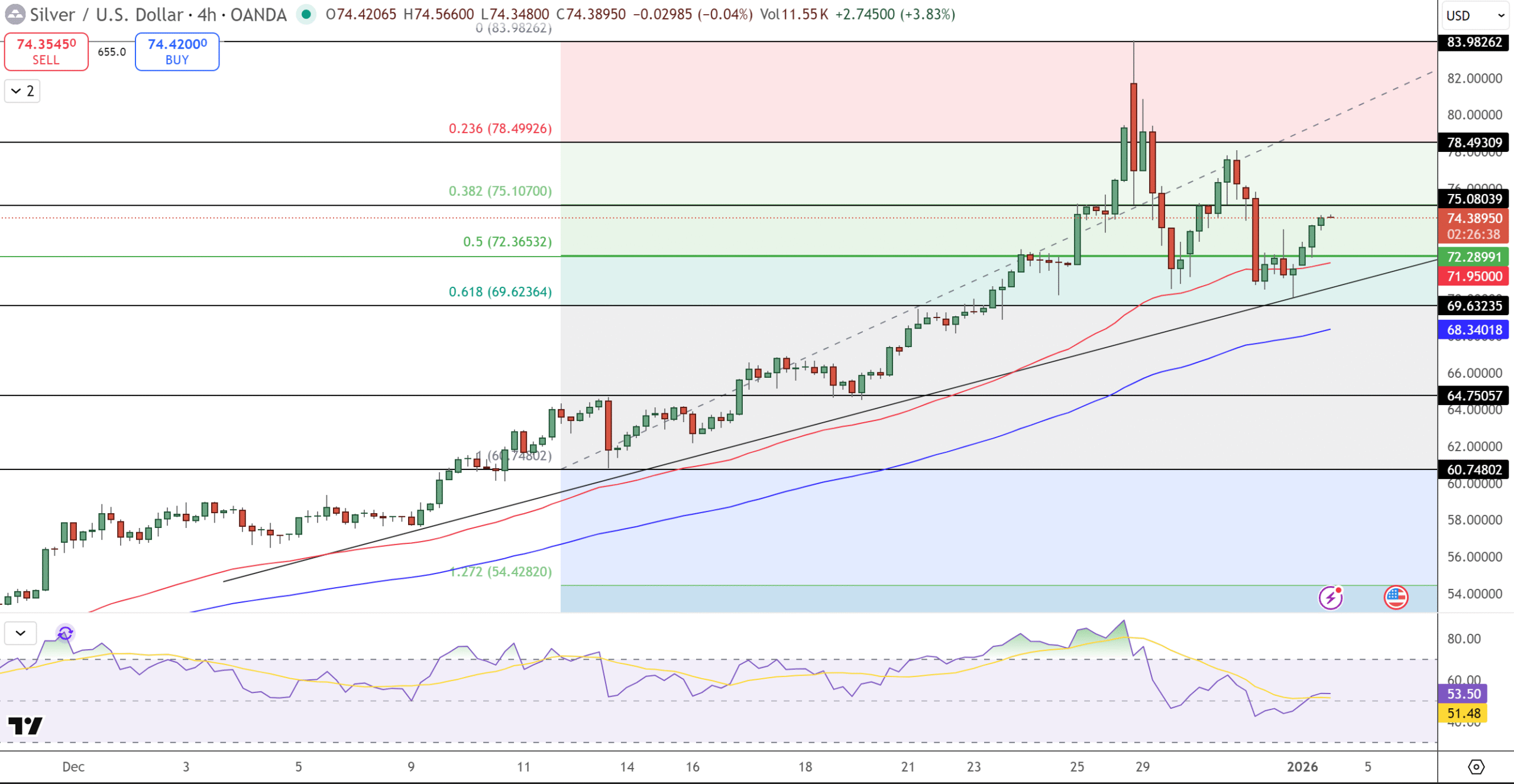

Other precious metals echoed gold’s early-year strength. Silver jumped 3% to $73.30 per ounce, building on a powerful 2025 performance driven by both safe-haven demand and industrial use. Consumption tied to renewable energy, electronics, and data centres has increasingly linked silver’s outlook to long-term infrastructure trends.

Platinum rose 2.5% to $2,102.30 per ounce, supported by tightening supply and improving industrial sentiment. In 2025, silver surged nearly 150%, while platinum posted gains of about 110%, underscoring the breadth of the precious-metals rally.

Base metals also edged higher. London copper futures gained 0.7% to $12,549.20 a ton, while U.S. copper futures rose 0.6% to $5.74 a pound, reflecting cautious optimism around global manufacturing demand.

As 2026 opens, precious metals remain underpinned by monetary easing, geopolitical risk, and structural demand, suggesting last year’s rally may be consolidating—not ending.